An Enquiry into the Velocity of Money & Cash-Flow

By Zak Klemmer

Copyright 2023 Tortolita West Holdings LLC

Tortolita West Holdings LLC wouldn’t exist as we would not be in business if we didn’t discover this principle and have the self-discipline to follow through with our personal behavior. Your results may be different than ours, if you follow through with what is outlined in this eBook, the principle should work for you too.

Cookie Cutter solutions? My frustration with the financial services industry is that I only delt with salespeople; it was only for thee and not for me. It was for the benefit of the business I was dealing with and their strategies were not necessarily for my benefit as a priority.

“It is hard to imagine a more stupid or more dangerous way of making decisions than by putting those decisions in the hands of people who pay no price for being wrong.” ― Thomas Sowell

Cash-Flow

I used to hate it when the first of the month arrived, it meant that my mortgage payment and my car payment were due and sometimes I didn’t have enough to pay them until the 10th or the month, and sometimes my mortgage payment wasn’t paid until the 15th of the month.

Let’s look at how the financial companies train their customers. Writers in social media, movies and TV take the cues from the Financial Services industry in crafting their stories and it has become second nature for the majority of the population here in America.

Segregation of Accounts:

Do you have any of the following?

Checking Account

Passbook Savings Account

IRA

401k

CD’s (Certificates of Deposit)

Mutual Funds

529 (College Savings Plans)

Treasury Securities

It’s been my experience talking to bank tellers and the managers at my bank that their goal is to sell to the bank’s customers the idea to open as many different types of accounts as possible. This is a segregation of accounts and puts the power into the hands of the institution and takes the decision-making power and advantage away from the customer. One example is right after we opened up a line of credit to purchase a rental property for Tortolita West Holdings LLC, I went into my bank to deposit a check and the teller started giving me a sales pitch:

“I’ve got great news Zak, we’re having a sale on One Year CD’s, If you open up a new account this month, (the bank’s name) will add a bonus of a quarter point of interest! Would you like to open a new CD?” I had just opened a line of credit and the interest paid on a One Year CD was less than what they were charging on my line of credit.

Discover the actual cost of credit:

Money is always for rent. When you apply for a new loan or a line of credit, you are entering into a contract to repay what you have borrowed or access to money on your available credit. The terms dictate your obligation and there is an advantage to a line of credit or a credit card which is revolving compared to an amortized loan. A revolving credit line or credit card, principal payments can be made and you can later draw from your available line or charge merchandise, the money goes around and around. A revolving credit line is simple interest, calculated on a daily basis and varies from month to month depending on your balance; you have the option paying the minimum (there is a calculation of principal and interest) on a credit card, interest only on a line of credit or HELOC. When you make a principal payment on your line of credit, you can access the available credit on the line later should you want to put the cash to work or have an emergency. Using the Velocity of Money Principle can save you money by arbitraging the difference between the interest cost of the amortization of your loan and the daily cost of your line of credit or credit card.

Arbitrage:

Arbitrage is the simultaneous purchase and sale of an asset in order to profit from a difference in the price. It is a trade that profits by exploiting price differences of identical or similar financial instruments on different markets or in different forms.

Amortized Loans have a built-in interest charge included in the monthly payment which are usually uniform during the course of the loan term. If you presently have a mortgage, the escrow officer or attorney would have given you the amortization schedule at closing. Mortgage companies profit more when you refinance your loan as most of the interest is front-loaded at the beginning of the loan term and as the note ages, more of the monthly payment goes to pay the principle balance. It take about 15 to 17 years before the portion of the payment which is applied toward the principal balance on a 30-year mortgage is greater than the interest portion. If you were to move after five years, or re-finance it starts the clock over and you are back at the beginning where most of the payment is going to interest. If you make a principle payment on a loan, you can’t draw against it the next week or in the future without re-financing, it just reduces your balance.

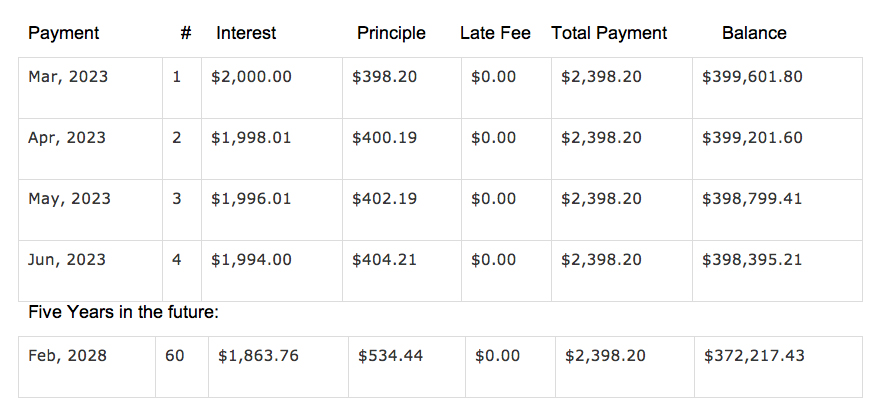

Example of a $400,000 – 30-Year fixed rate loan at 6% Interest:

After 60 months, your principal balance has only dropped by $27,782.57 after paying $ 143,892.00 in principal and interest.

After 30 years the amount of interest paid will be $ 463,349.21 and the total amount paid equals $ 863,349.21.

Another example is that a $400,000. Mortgage at a 5% Interest rate x 30-years fixed will be a total monthly payment of: $ 2,147.28, the amount of interest paid over 30 years will be $373,022.01 and the total amount paid equals $773,022.01.

A line of credit, a Home Equity Line of Credit (HELOC) or credit cards can be used to increase the Velocity of Money to shorten the time it takes to completely pay off your mortgage. Planning and implementing how you pay your bills each month and utilizing other credit accounts will accomplish this on your present income. This method can also be used to accelerate the payoff of any amortized loan, i.e., car loans, student loans, etc.

Our Experience

We started with a promotional zero interest credit card with a $10,000 credit limit. I would purchase everything with the card and keep all my cash in our checking account. Then I would chunk down larger than required principal payments to pay off the principal balance on our amortized loans, then chunk down the balance on the credit card. We bought another car with the card and carried the balance until the promotional period ended; completely paid off this card interest-free, paid off another promotional credit card interest free, and paid off the car loan at Prestige Financial. For our family, we recovered both our peace of mind and had more available cash in our checking account at the end of the month. A 769+ credit score for us was a bonus. We were approved for a HELOC and two mortgages.

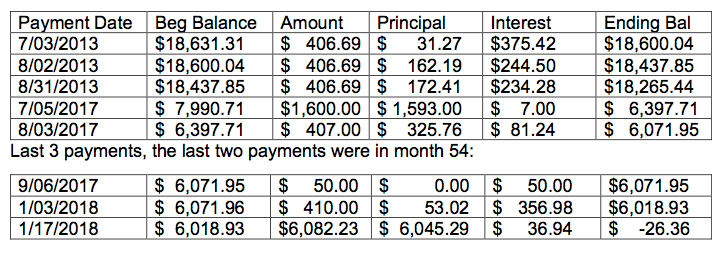

We eliminated most of our personal consumer debt. We started using Velocity of Money principles in 2017; we paid off a 72-month car loan in 54 months. The original amount financed was: $18,631.00. Our first payment was $406.69 of which only $31.27 went to principal and $375.42 was interest! After 48 months, we had paid: $ 19,521.12 in monthly payments and still owed $7,990.71. We made 2 substantial principal payments paying it in full in 54 months. We also paid off two credit cards at this time, an additional $13,000. This was in January of 2018.

72-Month Auto Loan at 16.5% Amortized Interest (Prestige Financial):

This eliminated 18 months of payments X 406.69 = $ 7,320.42 in my monthly cash-flow that I put to work. Then we paid off another loan balance of $4,900.00 – 16 months early which eliminated another monthly payment of $365. This strategy helped us eliminate over $959 in monthly payments in less time and saved us thousands of dollars.

Gain an understanding of the tools that banks, and credit card companies use to keep consumers tied up in monthly payments for years and how you can avoid them or use them to your advantage. You can’t save your way to wealth, and with inflation, it makes more sense than ever to begin using this method, along with self-discipline will immediately improve your cash-flow by utilizing existing banking tools and changing the flow of money in your life. Retire debt 4-5 times more quickly without increasing your income, needing a 2nd job, working overtime; and without going on a beans and rice diet. By using lines of credit rather than traditional amortized loans.

Learn how to budget and find existing cash-flow quickly in your own life, then use the existing banking tools you already have to start the Velocity flow of money process.

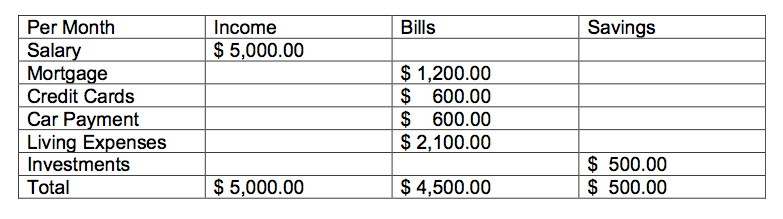

In the above budget example, let’s assume that:

The mortgage balance is $200,000 at a 6% amortized interest rate. Rule of thumb: take the rate X 2 = 12 X 10, the effective interest rate is closer to 116%.

The Credit Card has a balance of $16,000. And would take 27 years to pay-off making the minimum payments.

The Car Payment has a balance of $ 13,000. And would take 24 months to pay-off.

By changing the way the bills are paid with your current cash-flow, how great would it feel when you are debt free in 8.5 years? The strategy is to run the numbers and pay off the loans in a sequence that increases the free cash-flow, month after month, the fastest by using the available cash at the end of each month to pay the next loan. In this case, pay off the car loan, then the credit cards, then the mortgage. The math will tell you which loan will generate the most cash-flow quicker. In real life there are real figures and it would be simple to run the numbers.

How this works on your monthly budget:

Do you eat lunch out at work (take-out), or bring a lunch form home? A few dollars saved every day adds up over time.

Cheeseburger and Fries can set you back: $ 11 to $ 15

Pei-Wei Lettice and Chicken Wrap: $ 9

Restaurant Entrée: $ 10 to $ 12

Salad brought from home: $ 2 to $ 3

Think of the benefits putting this money to work paying down the principal balance on your mortgage, car loan, etc.?

1. Eliminate waste in your monthly budget/expenses; examine your habits. Magazine and other subscriptions that you have signed up for, online? Eliminating $5 per day X 30 days equals $150.00 per month. If it’s $10, then it’s $300.00. Is it worth extending your car loan or mortgage? Remember that every dollar that you save from paying interest is a tax-free return on your money!

2. What other ways with a close examination can you become more efficient and still enjoy your life-style?

3. List all your monthly obligations:

3.1 Credit Cards or loans with the highest interest rate?

3.2 Credit Cards or loans with the smallest balances?

3.3 Largest payments that you want to eliminate?

Find an Independent Insurance agent who will shop for you and advise you for the right coverages to fit your circumstances to mitigate risk.

Bank interest rates do not pay enough to keep up with inflation and it is taxable income. Using this method, in the above example, put the $500 that you were putting into savings (or the entire account balance); and use it to chunk down to pay-off either the credit card with the smallest balance or the highest interest rate. Do this repeatedly every month until you have eliminated the balances and all those monthly payments.

Use your available cash at the end of the month and make a payment against the principal balance on your line of credit or HELOC if you are using it as the account you are drawing against. Be sure to keep these accounts open and use them occasionally in the future as it will improve your credit score. The main goal is to increase the amount of available cash at the end of the month by eliminating your monthly payments. As your free cash-flow grows, you can increase the principal payments greater than the $500 that you started at the beginning! With a little planning using the above examples, it’s a snap!

Step 1: Use your available credit to move the cash to your checking account and make a principal payment on the first loan.

If you don’t have a HELOC or line of credit, use your credit cards to make purchases, use your cash to make the larger principal payments. It worked for us before we had a HELOC.

Step 2: Make principal payments at the end of the month with your available cash to your credit line.

Step 3: When you have restored your available credit to your line, draw against it and transfer it as cash into your checking account.

Step 4: Repeat step 1 until each loan or credit card is paid off and increase the payments as your end of the month cash-flow grows.

If you want to save time, you can automate your study to find out where your money has been spent. Intuit Corporation has a service that is online. The Mint. All you need to do is sign up for The Mint and enter in all of your accounts, and give it permission to pull in all the data from your accounts. If you feel uncomfortable giving it access, then you can use Microsoft Excel. Reference bankrate.com to research cost of credit.

My net-worth was not as important as my cash-flow when I was out of cash in my checking account. We used this system to get healthy financially, pay-off debt. We improved our credit score and started a business which continues to spin off cash every month. With self-discipline it can work for you as well.

Zak Klemmer, Realtor with United Real Estate Specialists

www.zakklemmer.com

Subscribe to my Real Estate Blog at: www.zakklemmer.medium.com

e-mail: zak@zakklemmer.net Cell: 520.358.4180